Bill Hillary Chelsea Clinton foundation fraud, Legal definition or just dictionary, Slush fund is misleading, Example on about page regarding 2013 consolidated financial reports, 88.4 percent spent on programs???

“the Democratic Party overlooked the ethical red flags and made a pact with Mr. Clinton that was the equivalent of a pact with the devil. And he delivered. With Mr. Clinton at the controls, the party won the White House twice. But in the process it lost its bearings and maybe even its soul.”…Bob Herbert, NY Times February 26, 2001

“The William J. Clinton Presidential Foundation, which reportedly expects to raise $200 million to build a library to help memorialize the ex-president’s legacy, is nothing more than a ‘slush fund,”…Dick Morris February 2001

Freedom is the freedom to say that two plus two make four. If that is granted, all else follows.”…George Orwell, “1984”

Fraud.

Corporate fraud:

“Activities undertaken by an individual or company that are done in a dishonest or illegal manner, and are designed to give an advantage to the perpetrating individual or company. Corporate fraud schemes go beyond the scope of an employee’s stated position, and are marked by their complexity and economic impact on the business, other employees and outside parties.”

Dictionary:

“an act of deceiving or misrepresenting”

The about page for the Bill Hillary and Chelsea foundation shows the following at the bottom:

2013 Expenditures (Per 2013 Consolidated Financials)

88.4%

Programs

7%

Management and General

4.6%

Fundraising

https://www.clintonfoundation.org/about

Gives one the impression that 88.4 percent of the expenditures went to the advertised end recipients doesn’t it?

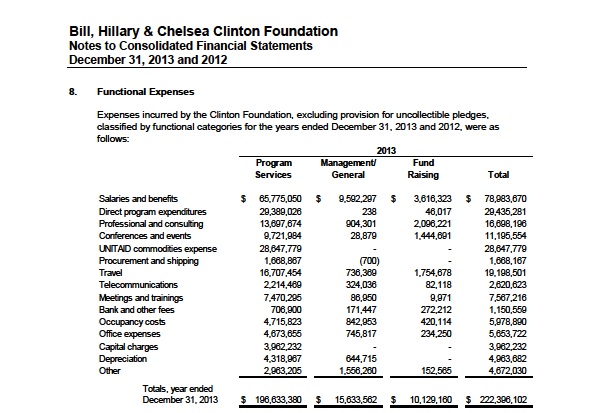

Here are the breakdowns for the expenditures:

Click to access clinton_foundation_report_public_11-19-14.pdf

That is a total of $ 222,396,102.

“Program services” $ 196,633,380.

Management general $ 15,633,562.

Fund raising $ 10,129,160.

The breakdown for “program services”.

Salaries and benefits……………… $ 65,775,050

Direct program expenditures……. 29,389,026

Professional and consulting………. 13,697,674

Conferences and events………………. 9,721,984

UNITAID commodities expense.. 28,647,779

Procurement and shipping…………. 1,668,867

Travel………………………………………. 16,707,454

Telecommunications…………………. 2,214,469

Meetings and trainings……………… 7,470,295

Bank and other fees…………………….. 706,900

Occupancy costs……………………….. 4,715,823

Office expenses…………………………. 4,673,655

Capital charges…………………………. 3,962,232

Depreciation…………………………….. 4,318,967

Other……………………………………….. 2,963,205

That is a lot of salaries, consulting, conferences, travel and meetings.

And those items total $ 113,372,457.

51 percent of total expenditures.

How did spending $ 113,372,457 help the advertised charity recipients.

Who benefited most?

I would like to to see the details.

From WND April 22, 2015.

“Wall Street analyst uncovers Clinton Foundation fraud”

“The Bill, Hillary, and Chelsea Clinton Foundation – already under scrutiny for foreign donations – is now being accused of fraudulent and possibly criminal mismanagement.

Over the past six weeks, Wall Street financial analyst and investor Charles Ortel has shared with WND, prior to publication, the results of his six-month, in-depth investigation into what he characterizes as an elaborate scheme devised by the Clintons to enrich themselves.

Through their foundation, Ortel contends, the Clintons have defrauded an unsuspecting international public of hundreds of millions of dollars for personal gain.

The findings come amid separate charges in Peter Schweizer’s upcoming book “Clinton Cash: The Untold Story of How and Why Foreign Governments and Businesses Helped Make Bill and Hillary Rich.”

In Ortel’s April 20 report, “False Philanthropy? First Interim Report Concerning The Bill Hillary & Chelsea Clinton Foundation,” he asks: “Did management exercise vigilance to ensure that the Clinton Foundation actually carried out its original and its amended tax-exempt purposes?””

““The numbers that the Clinton Foundation supply to the global public in its legally mandated filings do not add up, are frequently incorrect and overall appear to be materially misleading,” Ortel explained.

He said that in numerous cases, the Clinton Foundation “appears to have followed inconsistent policies adding in appropriate portions of the various activities it pursued around the world to create ‘consolidated’ financial statements.”

“In some instances, portions were added only for some of the years in which the entities remained in operation, artificially enhancing purported financial results,” Ortel concluded. “In other cases, important elements of activity were improperly characterized and combined.”

Ortel asks: “Do the Clintons, and others who operate the Clinton Foundation, function as Robin Hood in reverse – do they dupe small, modest income donors to enrich themselves and cronies?””

Read more: